01

The 30-second recap, then the part the short skipped

If you caught the short: the deal-killer isn't the price, it's the gap between "yes" on the call and money actually moving. People say yes when they're warm, then go cold the second they hang up — and now you're chasing an invoice that never gets paid. The fix isn't a better pitch. It's getting a tiny, almost-free commitment while they're still in the room: their card, on file, for a dollar. This guide is the whole play the 60 seconds couldn't fit — the exact Stripe link to build, the words to say so it doesn't scare them, and how you turn that dollar into the real subscription later without a second awkward money conversation.

Heads up on honesty: this is a sales process, not financial or legal advice, and not a tax or accounting opinion. Run your own offer, refunds, and terms past someone qualified before you put it live.

02

THE PSYCHOLOGYWhy this works: Olgaard's commitment-over-convincing heuristic

The thinking behind this is Albert Olgaard's — his heuristic is that you close with commitment, not convincing. His framing, in plain terms: the more you talk to overcome an objection, the more you signal the thing isn't worth it on its own. A small, real act of commitment does the opposite. Getting a card on file — even for a dollar — is that act. It quietly moves the buyer from "thinking about it" to "started," and a buyer who has started is one you stop having to chase. That's the whole reason for the dollar: it's not revenue, it's the smallest possible commitment that's still real.

- Convincing pushes against resistance — every extra argument is a little tell that the buyer should be cautious.

- Commitment is a small action the buyer takes themselves. Their brain backfills it as "I'm someone who's doing this."

- A $1 card-on-file is the minimum viable commitment: real money moves, so it's a genuine yes — but it's tiny enough that it doesn't trigger the "big purchase" alarm.

- Because it's framed as refundable and basically free, there's almost nothing to object to — so there's nothing to convince them out of.

Attribution so you can trust the rest: the commitment-over-convincing, card-on-file, and never-get-ghosted framing is Albert Olgaard's methodology — treat it as his heuristic, not a guaranteed outcome. We make no income, lifetime-value, or close-rate claims here; your results depend on your offer, your market, and you.

03

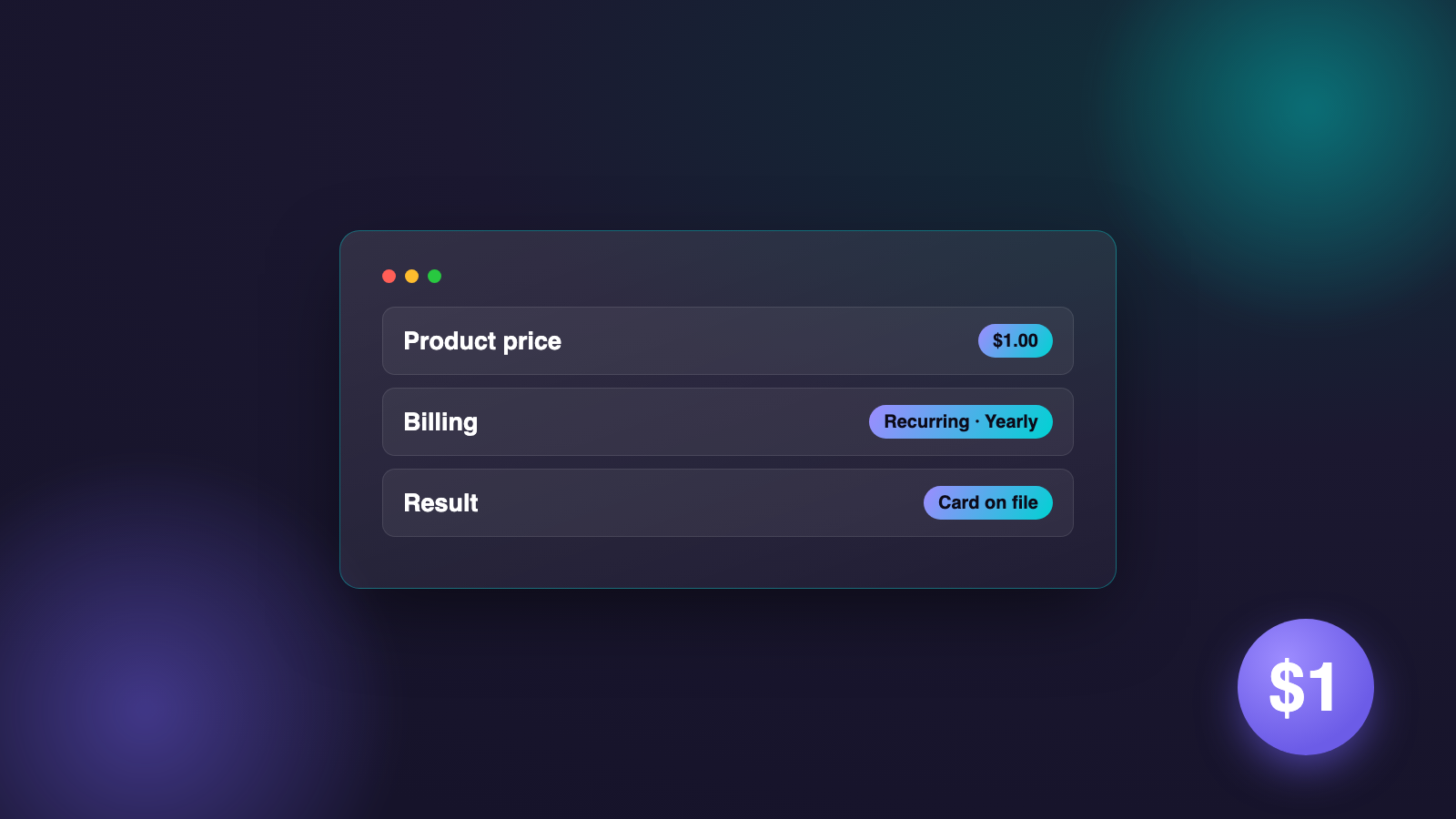

THE BUILD · 5 MINUTESStep 1 — Build the $1/year card-on-file link in Stripe

You want a Payment Link that charges a real $1, billed yearly, as a recurring subscription. That dollar is what puts a usable card on file. Be honest with yourself about what this is: Stripe Payment Links do not have a "save the card and charge $0" mode — a link either takes a real payment or it's a free trial (more on that next section). So the $1/yr is a real, tiny, refundable charge. Don't tell a buyer "this saves your card for free" — it doesn't; it charges a dollar. Here are the exact dashboard steps (naming verified against Stripe's docs on 2026-06-15):

- In the Stripe Dashboard, open the Payment Links page (

dashboard.stripe.com/payment-links). - Click + New (or the + and choose Payment link).

- Click + Add a new product. Name it something the buyer will recognize on their statement — e.g. "<Your Company> — Card on File" — so it never looks like a mystery charge.

- Set the price to $1.00, choose Recurring, and set the billing period to Yearly. (Recurring/yearly is fully supported on Payment Links — this is what makes it a stored, reusable card rather than a one-off.)

- Click Add product, then Create link. Copy the URL — that's the link you'll send the second they say yes.

- Optional but worth it: keep this product separate from your real plans, so your $1 card-on-file links never get tangled up with actual billing.

Why yearly and not monthly: a yearly $1 means you're not auto-charging them another dollar next month while the deal is still being set up — you've got a full runway to convert the commitment into the real subscription. The dollar's job is done the instant the card is stored.

04

IF YOU WANT ZERO CHARGEThe honest alternative: a true $0-now free-trial link

If charging even a dollar feels wrong for your buyer, Stripe has a genuinely $0-now path — and you should know it exists so you can choose on purpose. Make your real plan a subscription product, then on the Payment Link select "Include a free trial." During the trial, Stripe can collect and authorize the card without charging it (under the hood that's a SetupIntent — the card is verified and stored, $0 moves), and bills automatically when the trial ends. There's even a "let customers start trial without a payment method" option, but that defeats the whole point here — you want the card on file. So: pick the free-trial-with-card route if you need a literal $0, or the $1/yr route if you want the cleanest, most unambiguous "they put real money on it" commitment. Both are legitimate; just don't mix up the claims.

- $1/year recurring → a real, tiny, refundable charge. Strongest commitment signal; cleanest to explain ("a dollar, refundable").

- Free-trial subscription, card required → literally $0 now, card authorized + stored via Stripe's setup flow, auto-bills when the trial ends. Use when even $1 is a sticking point.

- Either way the outcome you care about is identical: a card on file, so the real charge later needs no new payment conversation.

Don't claim the $1 link "saves the card for free" — it charges a dollar. Don't claim the free-trial link charges anything now — it doesn't. Say exactly what each one does.

05

THE WORDSStep 2 — The close-call script that gets the card without the flinch

The card-on-file move lives or dies on framing. You are not asking for payment — you're asking them to start, with something refundable and basically free. Olgaard's point applies: the moment they take the small action, the deal is real. Say it plainly, name the dollar, name the refund, and go quiet. Here are word-for-word lines you can adapt to your voice — the brackets are yours to fill.

- Transition (right after the yes): "Perfect — let's get you started. The way I kick this off is I'll send you a link to put a card on file. It's a dollar, fully refundable, just so we're officially moving and I can hold your spot to start building."

- Reframe the dollar (if they pause): "To be clear, this isn't the [real price] — that comes once you've actually seen the work. This is just the commitment so I know you're in and I'm not building for someone who ghosts. A dollar. You can have it back any time."

- Send it live, on the call: "I'm texting / emailing you the link right now — it's literally one screen. Tap it while we're on, and we're off to the races." Then stop talking and let them tap.

- Confirm and set the next beat: "Got it — card's on file, you're officially started. Here's what happens next: [I build the first version by X / our call is booked for Y]. When it's ready, I flip your plan on — nothing else for you to do."

The discipline: name the dollar and the refund in the same breath, then go silent. Don't justify it, don't stack three more sentences — that's convincing, and convincing leaks doubt. The small ask only works if you treat it like the small thing it is.

06

THE CONVERSIONStep 3 — Spin up the real subscription later, zero friction

This is the payoff. Because the card is already on file in Stripe, switching them onto the real plan needs no second awkward money conversation — no new link to chase, no "so, about payment…" call. Here's the honest mechanism, not magic:

- Find the customer Stripe created when they paid the dollar — they're a real Customer object with a saved, reusable payment method attached.

- When the work's ready, create the real subscription on that same customer at your actual price. Because a default payment method is already stored, Stripe charges it automatically on the normal cycle — no new checkout for them to complete.

- The honest version of the conversation is a notice, not an ask: "Your first version's live — I've switched you onto the [plan] at [price], starting [date], on the card you already have on file. Anything you want changed, just reply." You're informing, because they already committed.

- Cancel or let the $1/year lapse so they're not paying a stray dollar on top — you only ever wanted it for the card, and now you have the real plan running.

Be straight with them that a real charge is coming and when — quietly switching someone from a dollar to a full price with no heads-up is how you earn a chargeback and lose the relationship. Commitment buys you a frictionless transition, not permission to surprise them.

07

THE BACKBONEStep 4 — Pair it with a guarantee so commitment beats convincing

The whole sequence rests on one promise that makes saying yes nearly free of risk: build first, refund if they hate it. This is what lets you ask for commitment instead of grinding through objections. If the buyer knows they can walk and get their money back, there's almost nothing left to argue about — so you don't have to convince, you just have to deliver. That's Olgaard's heuristic made concrete: a strong guarantee turns the close from a debate into a formality.

- Lead with the guarantee, not the price. "I'll build the first version. If you don't love it, you don't pay — full refund, no hard feelings." Now the dollar-on-file is obviously safe.

- Make the refund genuinely easy. A guarantee you make people fight for isn't a guarantee — and it shows. Easy refunds are cheaper than the deals you lose to fear.

- Let the work do the convincing. You committed them cheaply, you built something real, and the result closes the full price. The order matters: commitment first, proof second, payment third.

- Keep your promises specific and honest. "Love it or it's free" only works if you actually honor it. The guarantee is a trust instrument; spend it carefully.

Why commitment beats convincing, one more time: convincing fights the buyer's caution and loses slowly; commitment gives the buyer a tiny, safe action and lets their own follow-through close the deal. The $1 link, the script, the conversion, and the guarantee are four parts of that one idea.

Get the next build guide (and the free starter kit)

New AI build + sales guides, starting with the free AI Reseller Starter Kit. No spam, unsubscribe anytime.

By submitting you agree to our Privacy Policy & Terms. Unsubscribe anytime.

You're in — check your inbox to confirm.

Frequently asked questions

Does a Stripe Payment Link actually save a card without charging?

No — and don't claim it does. A Payment Link either takes a real payment or runs a free trial. The $1/year link makes a genuine (tiny, refundable) charge, and that's what stores a reusable card. If you want a literal $0 now, use a subscription product with "Include a free trial" — Stripe collects and authorizes the card during the trial (a SetupIntent) without charging it, then bills when the trial ends.

Why $1 a year instead of $1 a month?

The dollar's only job is to put a card on file. Billing it yearly means you won't auto-charge another dollar next month while you're still setting up the real plan — you get a full runway to convert the commitment, then you cancel or let the $1/yr lapse once the real subscription is live.

Isn't charging a dollar just to store a card a bit sneaky?

Only if you hide it. The method is honest by design: you say "it's a dollar, fully refundable, just so we're officially started," and you mean it. The dollar is a real, refundable commitment — not a trick. If even a dollar feels off for your buyer, use the $0 free-trial route instead.

How do I move them onto the real price without an awkward conversation?

Because the card is already on file, you create the real subscription on that same Stripe customer and it charges automatically. The conversation becomes a notice, not an ask: "Your first version's live — I've switched you onto [plan] at [price] starting [date] on the card you already have on file." Always give the heads-up; surprising someone is how you earn a chargeback.

Whose idea is the commitment-over-convincing close?

The psychology — commitment beats convincing, get the card on file, stop getting ghosted — is Albert Olgaard's methodology. Treat it as his heuristic, not a guarantee. We make no income, lifetime-value, or close-rate claims; your results depend on your offer and your market.

Is this financial or legal advice?

No. This is a sales process, not financial, legal, tax, or accounting advice. Get your offer, refund terms, and any subscription disclosures reviewed by someone qualified before you put it live, and follow Stripe's terms.

Sources · Stripe — Payment Links support recurring subscriptions (Docs) · Stripe — Create a payment link (dashboard steps: +New → add product → Create link) · Stripe — Free trials on subscriptions / collect card without charging (SetupIntent) · Stripe — Set up payment methods for subscriptions with no initial payment